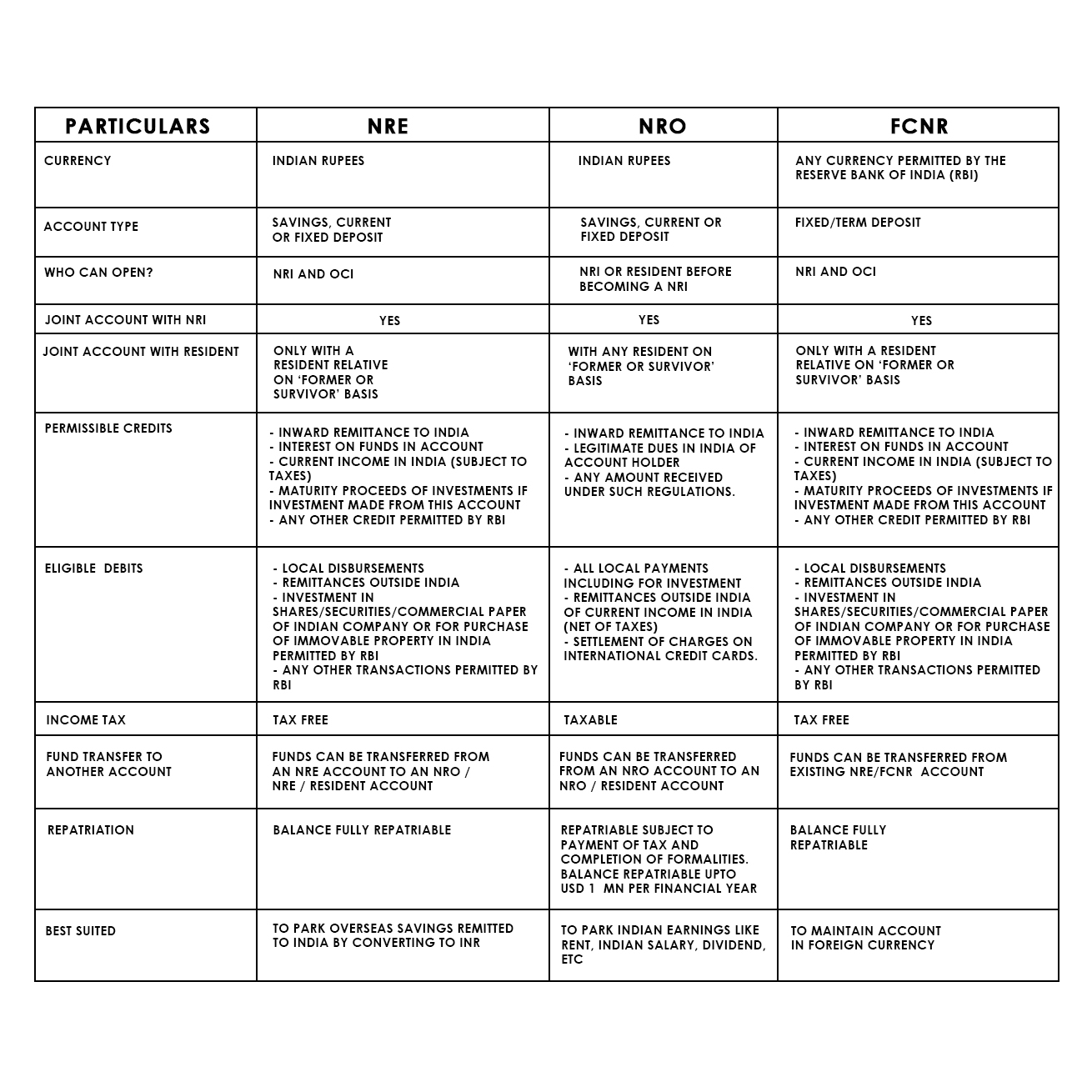

Introduction To NRO Account:

An NRO (Non-Resident Ordinary Account) account is a type of NRI account that is maintained in Indian Rupee. Through an NRO account, an NRI can manage all their incomes earned from India. An NRI can deposit their rent, dividend, interest, proceeds from the sale of assets, and various other incomes generated from India in their account. An NRO account is a savings account and it can also be used to make a fixed deposit. An NRO account can be opened jointly with a resident or a non-resident Indian.

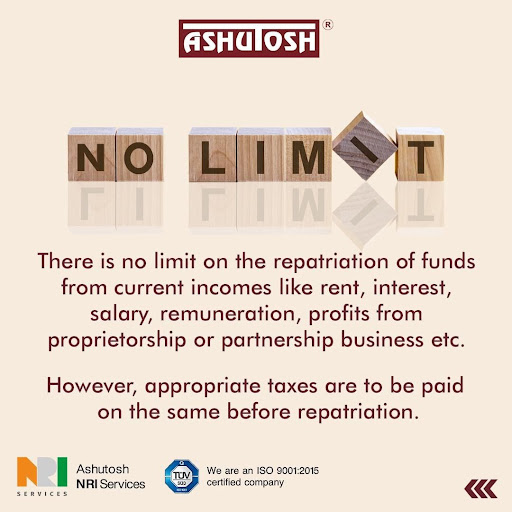

Any current income (rent, interest, dividends, etc.) received in an NRO account is fully repatriable after the payment of applicable taxes and completion of the necessary procedure. An NRI can also transfer up to $1 Million per year from their NRO account after paying the applicable taxes over and above the current incomes mentioned above. An NRO Account is immune to exchange rate fluctuations because it is a rupee-denominated account. An NRO account is always useful when it comes to investing in India.

People Eligible To Open An NRO Account:

- Non-Resident Indians (NRI).

- Person Of Indian Origin (PIO).

- Overseas Citizen Of India (OCI).

- Students Studying Abroad.

- Foreign Students Studying In India.

- Tourists On A Short Visit To India.

Benefits Of An NRO Account:

- Manage Indian Income: An NRO account helps the NRI in collecting and manage his Indian income. An NRI could have various types of incomes like Rent, Interest, and Dividends from their various investments in India. An NRI could also deposit the proceeds from the sale of Indian assets in this account. An NRO account lets an NRI deposit these incomes in their own NRO account in Indian Rupee denomination only.

- Immune To Currency Fluctuations: Most of the time the NRIs are at risk of losing money due to exchange rate fluctuations between the Dollar & Indian Rupee. An NRO account is immune to exchange rate fluctuations unlike an NRE account because it is a rupee-denominated account. Moreover, the repatriation of funds can also take place at the NRI’s discretion.

- Repatriation: An NRO account also allows the NRI to repatriate their Indian income to the country of their residence. It is important to note that an NRI can only transfer up to $1 Million in a financial year and that too after paying the applicable taxes on the gains made over and above the incomes like rent, interest, and dividends earned. This enables the NRI to keep receiving income from their investments in India in a streamlined manner.

- Investment: An NRO account also helps NRIs in investing in India. NRIs tend to invest in Indian stocks, mutual funds, and bonds for better returns. Since the NRO account is a rupee-denominated account, the NRIs can invest directly in the financial instrument of their choice without the need for conversion of currencies.

Better Returns: It is also common knowledge among the NRIs that since is a developing country, it offers better interest on saving accounts and fixed deposits. An NRI can therefore either park their surplus funds in fixed deposits or let it be idle in the savings account and earn interest. The interest earned however is taxable subject to TDS deduction as well. The interest amount is wholly repatriable only after paying the appropriate taxes.

Documents Needed To Open An NRO Account:

- Pan Card

- OCI Card

- Passport

- Bank Statement / Driving License (If OCI Card not available)

- Tax Identification Number

- Passport Size Photograph

How Can We Help You?

Ashutosh Financial Services Private Limited is a Rajkot-based company that has been serving the needs and requirements of NRIs. We provide NRI Services relating to Investments, Insurance, Income Tax Compliance, Foreign Tax Compliance, FEMA Regulations, Estate Planning, & NRI Banking. We have been providing all these NRI Services for over 20 years now. At Ashutosh Financial Services Private Limited we have a team of qualified and experienced individuals who have years of experience when it comes to dealing with the needs and requirements of the NRIs.

Any NRI willing to do a transaction to or from India needs to have an NRI Bank Account. It is very important to note here that a lot of NRIs would not have any idea about the banking regulations that they need to follow for opening an NRI Bank account or the types of bank accounts that an NRI can open. Since it is a very crucial part of the overall NRI Banking we at Ashutosh Financial Services have a process-driven approach that has been custom created to address the various needs of an NRI.

There are multiple types of NRI bank accounts that an NRI can open, we explain and outline all the advantages and disadvantages of these types of accounts. However, it is through detailed discussion that we identify and address the banking needs of an NRI and help the NRI in choosing the right type of bank account as per their need. We also help the NRIs in selecting a bank for opening their bank account. We not only guide the NRIs in the process of opening the bank account but also take regular follow-ups from the bank executives (if need be). Our aim is to provide the NRIs with a hassle-free experience while opening a bank account in India.